Table of ContentsEverything about Why Do Banks Sell Mortgages To Other BanksGetting The Which Fico Score Is Used For Mortgages To WorkThe Facts About What Are Jumbo Mortgages RevealedThe 7-Minute Rule for How Did Subprime Mortgages Contributed To The Financial CrisisSome Known Details About How Many Mortgages Can One Person Have

If you need to take a homebuyer course in the next couple of months, we advise the online course. Have concerns about purchasing a house? Ask our HUD-certified housing therapy team to get the responses you need today. what is the current interest rate for mortgages.

A lot of individuals's regular monthly payments likewise include extra amounts for taxes and insurance. The part of your payment that goes to primary minimizes the amount you owe on the loan and develops your equity. The part of the payment that goes to interest does not decrease your balance or build your equity. So, the equity you develop in your house will be much less than the amount of your regular monthly payments.

Here's how it works: In the start, you owe more interest, because your loan balance is still high. So the majority of your regular monthly payment goes to pay the interest, and a little bit goes to paying off the principal. In time, as you pay down the principal, you owe less interest monthly, because your loan balance is lower.

Near the end of the loan, you owe much less interest, and many of your payment goes to settle the last of the principal. This procedure is called amortization. Lenders use a standard formula to calculate the month-to-month payment that permits just the correct amount to go to interest vs.

What Are Adjustable Rate Mortgages Fundamentals Explained

You can utilize our calculator to compute the regular monthly principal and interest payment for different loan quantities, loan terms, and rates of interest. Idea: If you're behind on your mortgage, or having a difficult time making payments, you can call the CFPB at (855) 411-CFPB (2372) to be connected to a HUD-approved real estate counselor today.

If you have an issue with your home mortgage, you can submit a problem to the CFPB online or by calling (855) 411-CFPB (2372 ).

Probably among the most confusing things about home loans and other loans is the calculation of interest. With variations in compounding, terms and other factors, it's hard to compare apples to apples when comparing home mortgages. Sometimes it appears like we're comparing apples to grapefruits. For instance, what if you wish to compare a 30-year fixed-rate home loan at 7 percent with one indicate a 15-year fixed-rate home mortgage at 6 percent with one-and-a-half points? Initially, you need to keep in mind to likewise consider the fees and other costs associated with each loan.

Lenders are needed by the Learn here Federal Fact in Financing Act to disclose the reliable portion rate, in addition to the overall financing charge in dollars. Advertisement The yearly percentage rate (APR) that you hear so much about permits you to make real comparisons of the actual costs of loans. The APR is the typical annual finance charge (that includes fees and other loan costs) divided by the amount obtained.

Some Known Facts The original source About Who Does Usaa Sell Their Mortgages To.

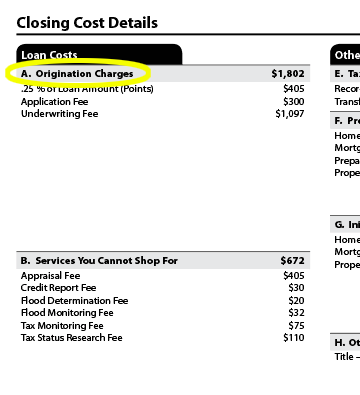

The APR will be a little higher than the rate of interest the lender is charging since it includes all (or most) of the other costs that the loan carries with it, such as the origination charge, points and PMI premiums. Here's an example of how the APR works. You see an advertisement offering a 30-year fixed-rate home loan at 7 percent with one point.

Easy choice, right? Really, it isn't. Fortunately, the APR considers all of the small print. State you require to obtain $100,000. With either loan provider, that means that your monthly payment is $665.30. If the point is 1 percent of $100,000 ($ 1,000), the application charge is $25, the processing cost is $250, and the other closing costs amount to $750, then the total of those charges ($ 2,025) is subtracted from the actual loan quantity of $100,000 ($ 100,000 - $2,025 = $97,975).

.jpg)

To discover the APR, you determine the interest rate that would equate to a regular monthly payment of $665.30 for a loan of $97,975. In this case, it's really 7.2 percent. So the second loan provider is the much better deal, right? Not so fast. Keep reading to discover the relation between APR and origination charges.

A mortgage or merely mortgage () is a loan utilized either by buyers of genuine property to raise funds to purchase property, or alternatively by existing homeowner to raise funds for any function while putting a lien on the property being mortgaged. The loan is "protected" on the customer's residential or commercial property through a procedure called home mortgage origination.

5 Easy Facts About How Many Mortgages Can You Have At One Time Described

The word home mortgage is stemmed from a Law French term used in Britain in the Middle Ages indicating "death promise" and refers to the pledge ending (dying) when either the responsibility is fulfilled or the home is taken through foreclosure. A mortgage can also be described as "a customer giving consideration in the form of a security for a benefit (loan)".

The lender will generally be a financial institution, such as a bank, credit union or developing society, depending upon the country worried, and the loan plans can be made either directly or indirectly through intermediaries. reverse mortgages are most useful for elders who. Functions of home loan such as the size of the loan, maturity of the loan, rate of interest, technique of paying off the loan, and other attributes can vary substantially.

In numerous jurisdictions, it is regular for house purchases to be moneyed by a mortgage loan. Few people have sufficient cost savings or liquid funds to enable them to acquire home outright. In countries where the need for own a home is highest, strong domestic markets for home loans have established. Mortgages can either be funded through the banking sector (that is, through short-term deposits) or through the capital markets through a procedure called "securitization", which converts pools of mortgages into fungible bonds that can be offered to financiers in little denominations.

For that reason, a mortgage is an encumbrance (constraint) on the right to the property simply as an easement would be, but because many home mortgages occur as a condition for brand-new loan money, the word home loan has become the generic term for a loan secured by such real property. Similar to other kinds of loans, mortgages have an interest rate and are set up to amortize over a set time period, generally 30 years.

Examine This Report about Who Does Usaa Sell Their Mortgages To

Mortgage financing is the main mechanism utilized in many nations to fund personal ownership of domestic and business home (see commercial home mortgages). Although the terminology and precise forms will vary from country to nation, the standard elements tend to be similar: Property: the physical residence being funded. The exact type of ownership will vary from nation to country and might restrict the kinds of loaning that are possible. reverse mortgages how they work.

Restrictions may consist of requirements to buy house insurance coverage and mortgage insurance, or settle impressive financial obligation prior to selling the home. Borrower: the individual borrowing who either has or is creating an ownership interest in the residential or commercial property. Lender: any loan provider, but usually a bank or other banks. (In some nations, especially the United States, Lenders may also be investors who own an interest in the home mortgage through a mortgage-backed security.

The payments from the customer are thereafter gathered by a loan servicer.) Principal: the initial size of the loan, which might or might not include certain other costs; as any principal is paid back, the principal will go down in size. Interest: a financial charge for usage of the lender's cash.